SaaSpocalypse: Why the Market Torched $300 Billion in Software Stocks, and How to Determine Who Deserves It

SaaSpocalypse: Why the Market Torched $300 Billion in Software Stocks, and How to Determine Who Deserves It

In early 2026, the software sector lost roughly $300 billion in market cap across about six weeks. Lots of people called it a panic. It wasn't. The selloff followed a clear and coherent logic about which software businesses AI threatens and which it doesn't.

The 8-Question Diagnostic

If you’re a SaaS company leader or an employee, or an investor in SaaS companies you are likely looking for a way to strategically assess a company’s strengths and weaknesses in relationship to AI. We distilled the best frameworks from a range of sources (see Sources and Frameworks) into eight questions you can score 1 to 5 for any company:

Is the core function deterministic or probabilistic? Deterministic functions (authentication, payment processing, compliance calculations) must be exactly right; probabilistic functions (content generation, task management, recommendations) are precisely what AI produces natively and cheaply.

What happens in the physical world if this software fails? Software embedded in physical operations (restaurants going dark, construction sites stalling, payroll not running) is much harder to displace than software where failure just means someone opens a different tab.

Does an AI agent need this product to function, or does it compete with it? Identity providers, databases, and security tools are inputs that AI agents call into; task managers, engagement layers, and guided interfaces are outputs that AI agents produce directly.

How deep is the data gravity, and who controls the data? A decade of proprietary records, custom configurations, and integrations creates migration costs that protect revenue even when the product isn't best-in-class anymore.

Does this company sit above or below the "agent layer" in the emerging stack? Software below the agent layer (infrastructure, databases, network plumbing) gets called by AI agents; software above it (dashboards, wizards, UIs) gets replaced by them.

How does AI change the unit economics of this company's customers? If AI lets customers do the same work with fewer employees, per-seat revenue contracts automatically even if nobody cancels; if AI increases the volume of transactions or events the customer processes, consumption-based revenue grows automatically.

What is the regulatory or compliance moat, and is it deepening or shallowing? Industries where software errors trigger audits, fines, or liability (FDA, banking regulators, OSHA) create non-discretionary spending floors that AI substitution can't easily erode. New AI regulation is creating more of these protected categories.

Is the company's revenue model aligned with or misaligned with the AI transition? Per-seat models lose revenue when AI reduces headcount; transaction, consumption, and outcome-based models grow revenue when AI drives more activity through the platform.

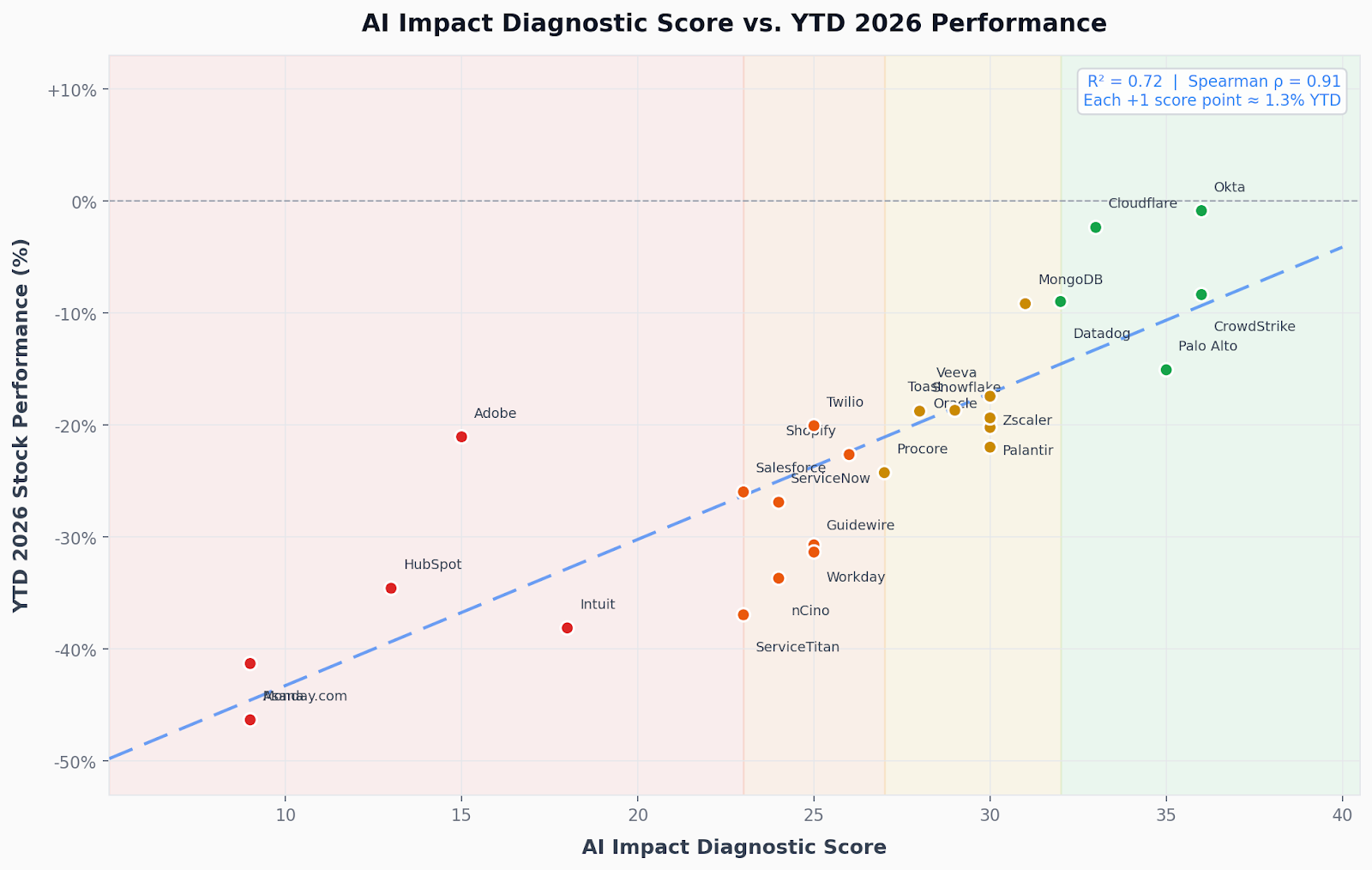

Depending on how you scored your business across these dimensions, you may have identified strengths to build on (i.e. being a source of truth system or a system that AI agents rely upon) or weaknesses that need to be shored up (i.e. revenue model misalignment or limited AI usability). Scored To illustrate, we scored 26 public companies. These eight questions explain 72% of the variance in YTD 2026 stock performance as of February 18th (Pearson r = 0.85, Spearman ρ = 0.89). Each additional point on the rubric corresponds to roughly 1.3 percentage points of better stock performance. The chart below shows the relationship:

The color bands (green for scores 32+, yellow 27–31, orange 23–26, red below 23) correspond to roughly four tiers of outcomes: down less than 10%, down 15–25%, down 25–35%, and down 35%+.

By the way, we discussed the SaaSpocalypse framework on our new podcast, Eventual Consistency. Check out the episode here.

Four Companies That Illustrate the Framework

Four companies (Okta, Workday, Salesforce, and Shopify) sit at very different points in the matrix and tell very different stories.

Okta is the cleanest possible illustration of the "AI needs this" thesis. It scored 5 out of 5 on three of the eight questions, which is essentially saying AI is a direct tailwind on those dimensions. Here's why:

Determinism (5/5): Authentication is binary. Access is either granted or denied. There is no "approximately authenticated." This is exactly the kind of deterministic execution layer that AI agents need to act against, not a function AI replaces.

AI needs it, not competes (5/5): Every AI agent deployed in an enterprise needs identity credentials, permission scoping, and an audit trail. You can't have an AI agent accessing customer data without authenticating through an identity provider. More agents = more Okta usage. This is the textbook "picks and shovels" play.

Below the agent layer (5/5): Agents authenticate through Okta, not around it. The company sits definitively in the infrastructure layer below where agents operate.

Demand expansion (5/5): Each new AI agent is a new identity to manage. The addressable market grows automatically with AI adoption.

36/40 is the highest score in the analysis alongside CrowdStrike. A -0.9% YTD in a sector where most stocks are down 20-40% speaks for itself.

Toast (Score: 29/40, YTD: −18.7%): When the POS Goes Down, the Restaurant Goes Dark

Toast is the clearest illustration of what "physical world consequences" actually means for AI durability, and why it matters so much in the diagnostic. It scored 5/5 on Q2, which is the highest in the yellow band and higher than most companies in the green band:

Physical world consequences (5/5): If Toast fails, the restaurant cannot take orders and payments cannot be processed. This is the Vendep Capital "flow of money and physical goods" thesis: software that, when it fails, causes a physical business to halt is not easily substituted.

Revenue model alignment (4/5): Transaction-based revenue means every card swipe is a Toast revenue event. AI-driven ordering surfaces (conversational AI, voice ordering) don't replace the payment rail; they feed into it. More ways to order means more transactions, not fewer.

Determinism (4/5): Payment processing is binary. A charge either clears or it doesn't. "Approximately correct" payment processing is not a concept that exists.

Below the agent layer (4/5): The hardware terminals and payment infrastructure sit definitively below any agent orchestration layer. AI can improve demand forecasting and menu optimization without touching the POS.

Mixed AI relationship (3/5): This is Toast's ceiling. AI can enhance scheduling, marketing, and back-office modules, but it can also compete with them. The payment and hardware foundation scores well; the software-only modules score more like workflow tools.

The −18.7% YTD result reflects exactly this structure: a very strong physical/payments foundation holding up software modules that are more exposed than the blended score suggests.

Salesforce (Score: 23/40, YTD: −26.0%): Maximum Data Gravity, Structural Headwinds Everywhere Else

Salesforce is the most interesting case in the entire analysis because it has the deepest data gravity of any company we scored (a 5/5) and is still down 26%. That tells us that even the strongest moat on one dimension can't compensate when you have weaknesses across most of the others.

Data gravity (5/5): A decade of customer records, custom objects, Apex code, and thousands of integrations. IDC research shows organizations with 10+ Salesforce integrations have 40% lower churn. The data isn't going anywhere.

Determinism (3/5): CRM data storage is deterministic; lead scoring, forecasting, and engagement recommendations are probabilistic. Mixed.

AI needs it vs. competes (3/5): This is the crux of the Salesforce problem. Satya Nadella described business applications as "essentially CRUD databases with a bunch of business logic... the business logic is all going to these agents." AI agents need Salesforce's data (positive) but bypass the CRM UI entirely to get it (negative). AgentForce (which hit $540M ARR at +330% YoY growth) is Salesforce's bet to stay relevant at the agent orchestration layer rather than getting disintermediated.

Below the agent layer (3/5): Salesforce is betting on being at the agent layer via AgentForce rather than being bypassed as a dumb data store. Whether that succeeds is the central question for the stock.

Demand compression (2/5): If AI handles 40% of sales tasks, you need fewer seats. And hyperscalers spending $470B+ on AI capex in 2026 means IT budget is moving away from SaaS renewals before it ever reaches Salesforce's renewal conversation.

Revenue model (2/5): Primarily per-seat licensing. Salesforce introduced its AELA (Agentic Enterprise License Agreement) concept, but the pricing model remains misaligned with a world where AI agents do the work. Kyle Poyar's data shows pure seat-based pricing dropped from 21% to 15% of companies in 2025 alone, and IDC predicts it's obsolete by 2028.

The lesson from Salesforce is that data gravity is necessary but not sufficient. You can have irreplaceable data and still face severe structural headwinds if AI competes with your interface, compresses your seat count, and your pricing model doesn't adapt.

Intuit (Score: 18/40, YTD: −38.1%): The Purest Substitution Story in the Dataset

Intuit is the company in this analysis where AI most directly competes with the core product value proposition. TurboTax guides people through tax preparation. AI also guides people through tax preparation. That's the whole problem:

Demand compression (1/5): The lowest possible score on the question that matters most for Intuit. AI can handle a basic tax return. The IRS Direct File program handles simple returns for free. Claude and GPT-4 answer specific tax questions more conversationally than TurboTax's step-by-step wizard does. This is not a future threat: it's happening now.

AI needs it vs. competes (2/5): For TurboTax specifically, AI is not a tool you use inside the product. AI is a competing product for the same job. The underlying tax calculation still needs to be correct (which keeps Q7 at 3), but AI reads the tax code too, and it doesn't charge a per-filing fee.

Revenue model alignment (2/5): Per-filing subscription under direct pressure from free alternatives. TurboTax Live (adding human CPA review) is a reasonable defensive move, but it competes with AI at the low end and professional accountants at the high end simultaneously.

Agent layer position (2/5): TurboTax is a guided UI for a task that AI agents handle natively. It sits above the agent layer almost by definition.

Partial protection from QuickBooks (3/5 on data gravity): Years of business financial records in QuickBooks are genuinely sticky in a way that annual tax filings are not. This is the floor that keeps Intuit from scoring like Monday.com.

At 18/40 and −38.1% YTD, Intuit looks nearly as bad as the horizontal workflow tools, but from a more defensible starting position. The QuickBooks franchise isn't finished. The TurboTax consumer franchise is what the market is increasingly pricing as structurally threatened.

Side Note: The Three Forces Hitting Demand

There are three distinct mechanisms by which AI disrupts SaaS demand, and conflating them produces bad analysis.

Seat compression: AI lets the same team do more with fewer licenses. Klarna went from 5,000 to 3,800 employees. Publicis reportedly reduced SaaS licenses by roughly 50%. Revenue per customer declines even as the relationship persists.

Vendor consolidation: Organizations reduce their total SaaS vendor count, canceling marginal or overlapping tools entirely. BetterCloud data shows average SaaS apps per company declined 18% in 2025, with 82% of companies actively reducing vendor count.

Budget reallocation: IT budgets are roughly flat. Hyperscalers are spending $470B+ on AI capex in 2026. Every dollar going to GPU compute and AI APIs is a dollar not available for SaaS renewals. As Lemkin put it: "AI isn't eating the product. It's eating the budget."

The worst-performing companies in the analysis are usually facing all three simultaneously.

The Honest Summary for SaaS Businesses

The framework points to a pretty clear checklist of what protects a SaaS business in the post-AI landscape:

Core function is deterministic (must-be-right, not good-enough)

Failure has physical-world or compliance-mandated consequences

AI agents need your product to function rather than compete with it

You sit below the agent layer, or have a credible plan to sit at it

Deep data gravity (years of proprietary records, painful to migrate)

Strong regulatory or compliance moat that is deepening with new AI regulation

Revenue model based on consumption, transactions, or outcomes rather than seats

Companies hitting most of these are down less than 10% YTD. Companies hitting few or none are down 35-46%.

The uncomfortable implication is that the most exposed category (horizontal workflow and creation tools on per-seat pricing without meaningful data gravity or compliance requirements) is also one of the most crowded parts of the SaaS market. Monday.com (−46.3%) and Asana (−41.3%) aren't anomalies. They're the clearest signal the market has sent about what generic human-task-management software is worth in a world where AI manages tasks natively.

If any of this sounds familiar, we would be glad to help you work out what your stack needs to ride the AI wave rather than being washed out by it. Reach out here.

.png)

.jpg)

.jpg)